3 minutes

With Covid-19 impacting the cash reserves, financial breathing space and bank balances for SMEs, business advisory and finance professionals firm, Edale share their five key financial statements that smaller company leaders should be aware of in 2021.

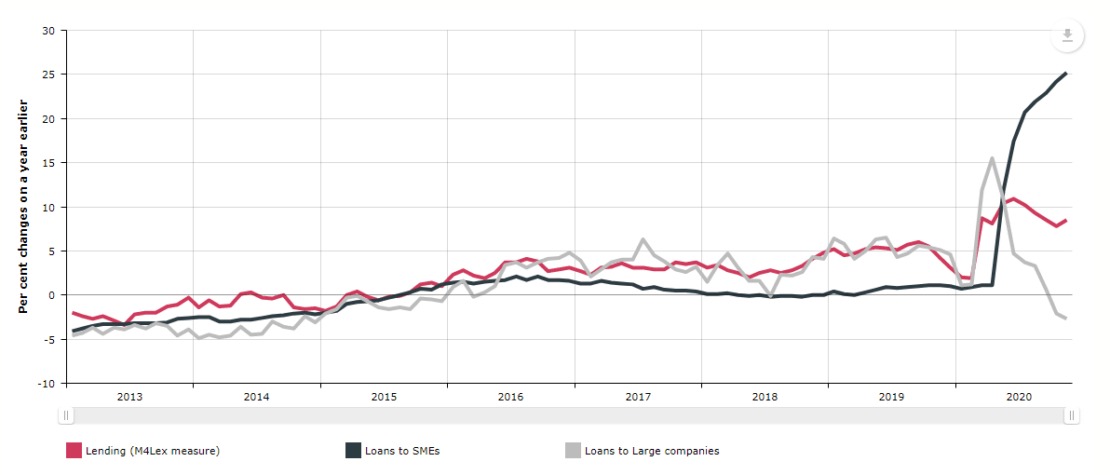

1. Financial stress for smaller businesses continues to rise

Loans to smaller companies have continued to grow, at the last data point they were 25% higher than the previous year. While lending to larger companies appears to have peaked in April 2020 due to emergency funding, it’s now peaked and retrenching. Smaller companies continue to be under financial stress and seeking loans at record levels.

2. Financing during COVID19 is different in 2021 to 2020

Financial needs in 2020 were very much based on the emergency funds from public authorities. However, this year business leaders are being encouraged to focus on the 3Rs – Resilience, Recovery and Response. Different language and perception is meaning some of the bounce back responses are being extended but with firmer sunset dates. With that in mind, bounce back funding should be considered as low cost funding and a potential source of finance to help move your business forward.

3. Revenue and profit are different from cash flow and working capital

When starting a business, it’s easy to get confused about the difference between revenue, profit and cash flow. Many believe that businesses fail because of no sales or low profit, when in reality they fail because they run out of cash. If cash is available in the business, short term dips in profit and revenue can be survived. Let’s break it down:

-Revenue = sales that come in / the amount that you invoice for

-Profit = the difference between what it costs to bring the service or product in, run your operation and the amount you sell it for.

-Cashflow = the timings and flow of cash.

When money is deposited into your bank account or given to you as cash, it is considered an inflow. Where as when you pay an expense and the money leaves your bank account, it is considered an outflow.

The aim is to maximise the size and timing of inflows and minimise the size or delay outflows – this is called the ‘raised eyebrow’ concept and can be seen in the example charts below.

4. Securing financial support can take time

It’s important to remember that securing financial support in the form of grants or loans can be difficult with paperwork, processes and required checks making it a long process. The good news is, there’s initiatives out there like the Bounce Back Funding Programme that can help you get-going and ensure applications are completed correctly to avoid further delays. If you’re looking for a quick solution to increase revenue, we suggest re-evaluating your current offering and looking at new ways to adapt your products and services to make them more appealing to the target market, for example repackaging.

5. Testing a solution is hard alone

Not all solutions, adaptations or ideas come naturally, sometimes support is the best way to coax ideas out. When looking for business recovery assistance, you don’t necessarily need an accountant, lawyer or coach, instead look for collaborative support that is action oriented and outcome driven. Consider solutions such as technology to reduce admin, adopting a lean task management approach and getting a rapid grasp of commercial opportunities.

If you’re an established SMEs or incorporated non-profits in the creative, cultural, heritage or digital sector that’s based in the Tees Valley, join us on the Creative Fuse Tees Valley Bounce Back Funding programme for support on harnessing financial resources and support.